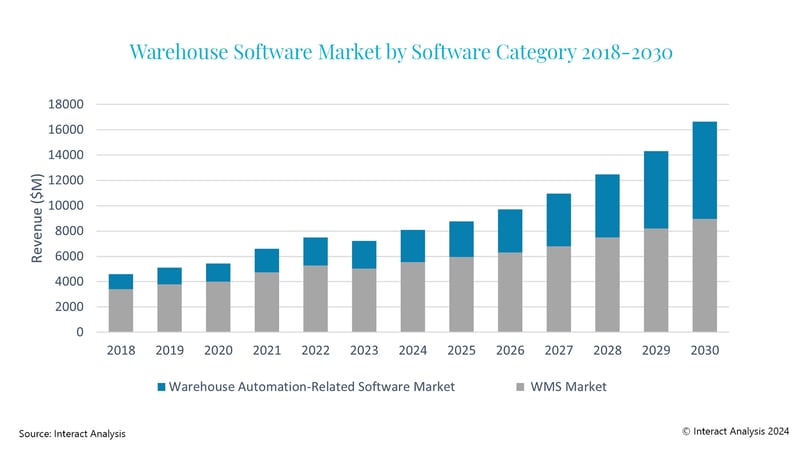

Warehouse software market valued at $7.2bn in 2023

- Warehouse software market to grow at a CAGR of 12.7% out to 2030

- The standalone warehouse management system (WMS) market remains the largest, but other warehouse automation-related software is growing exponentially

- Warehouse Execution Systems (WES) are being deployed as a strategic choice to increase operational efficiency

According to the latest research by market intelligence firm Interact Analysis, the warehouse software market is facing a rapid growth trajectory. In 2023, the market was valued at $7.2 billion, and this is expected to soar to $16.6 billion by 2030.

Exponential growth of warehouse automation-related software

Overall, the standalone WMS remains the largest software category. The markets for other warehouse automation-related software, such as robotic picking software, multi-fleet orchestration platforms, and warehouse control systems (WCS), are expected to grow rapidly and at a higher growth rate than the total warehouse software market. The automation-related software segment will expand at a compound annual growth rate (CAGR) of approximately 19.5% between 2023 and 2030, compared with 12.7% for the warehouse software market as a whole. The boundaries between different types of warehouse software vendors have become blurred as vendors expand their software product offering. Many traditional WMS vendors have started to offer WES and WCS solutions, for example.

WES deployed to enhance efficiency

According to Interact Analysis’ latest study, the deployment of a WES is a strategic choice leading to increased operational warehouse efficiency. Not only does the system provide visibility into warehouse asset operations but it also has the capability to dynamically release orders and assign tasks based on the real-time operation status of assets. As a result, bottlenecks can be avoided, and efficiency is increased. The WES data can also be used to predict future warehouse automation and capacity efficiency while providing feedback to warehouse managers.

However, the biggest question surrounding the WES market isn’t the benefits of the solution, but rather who will be providing it. Historically, automation vendors have been the main provider of WES solutions, given the amount of data they have on throughput rates and system constraints. However, we’re seeing strong growth in stand-alone WES solutions (independent of the WCS and the WMS) and Embedded WES solutions (where the WES is embedded into the WMS).

However, the biggest question surrounding the WES market isn’t the benefits of the solution, but rather who will be providing it. Historically, automation vendors have been the main provider of WES solutions, given the amount of data they have on throughput rates and system constraints. However, we’re seeing strong growth in stand-alone WES solutions (independent of the WCS and the WMS) and Embedded WES solutions (where the WES is embedded into the WMS).

The next few years will be highly dynamic, as different groups of companies compete to provide orchestration and execution capabilities. This report provides a wealth of information to help companies stay ahead of the curve in the race to own the execution layer.

Irene Zhang

Irene Zhang, Senior Analyst at Interact Analysis comments on the warehouse software growth trajectory, “The exponential growth of the warehouse automation-related software segment we have observed is the result of a few key drivers.

“First of all, the growth of warehouse automation has created the need for software that can be used to control and execute solutions. There is also a need to optimize the overall throughput due to the growth of modular and standardized automation sub-systems which require orchestration and execution of various modules. Finally, the growth of the mobile robot market has driven demand for fleet management systems. As well as this, the availability of the Robotics as a Service (RaaS) model has also contributed to the widespread adoption of mobile robots.”